Measuring the status of audit documentation indicators by using Internet-based technologies

Keywords:

Audit documentation, Internet-based technologies, Large scale data, Information Technology, audit qualityAbstract

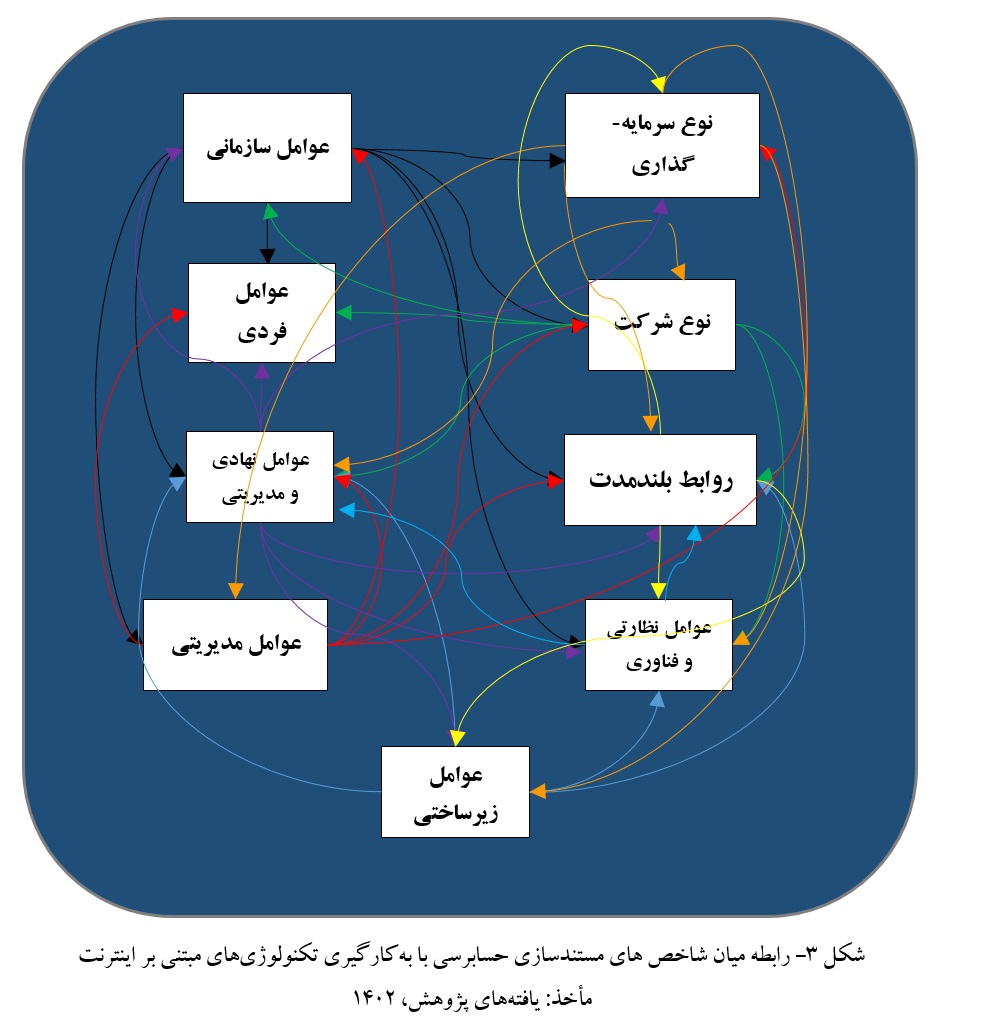

Currently, the lack of a comprehensive model regarding the use of Internet-based technologies in the formation of auditors' work is clearly felt. In fact, the main problem of this research is the necessity of an all-round look at the potential applications of Internet-based technologies on the formation of auditors' work; Because in most of the previous researches, it has only been proved that digital technologies have a positive effect on audit performance, and issues such as background factors, intervening factors, and strategies necessary for implementing digital technologies in the field of auditing have received less attention. The purpose of the current research is to measure the status of audit documentation indicators using Internet-based technologies. The current research is descriptive-analytical in terms of method and practical in terms of purpose. Fuzzy Dimetal and Fuzzy ANP techniques have been used for data analysis. The results obtained from Dimetal Fazi have shown that the influence of the index of "organizational factors" on audit documentation using Internet-based technologies is more than other indicators and the index of "management factors" is the next priority. . Also, the effectiveness of the "regulatory factors and technology" index is more than other indices. Also, the results of fuzzy ANP have shown that the index of organizational factors is in the first priority, the index of long-term relationships is in the second priority, and the rest of the indicators are in the third priority.

Downloads

References

Auditing Standard, A. (2007). Documentation, Revised 2007: Effective for auditing financial statements for financial

periods starting from April 1, 2007, and thereafter.

Delbari Raghb, M., & Ismailzadeh Moghri, A. (2023). Independent Audit Quality Model Emphasizing Stakeholder

Needs. Financial Accounting and Auditing Research, 15(1), 69-98. https://acctgrev.ut.ac.ir/article_88664.html

Gonçalves, M. J. A., da Silva, A. C. F., & Ferreira, C. G. (2022). The Future of Accounting: How Will Digital

Transformation Impact the Sector? Informatics, 9(1), 19. https://doi.org/10.3390/informatics9010019

Guşe, G. R., & Mangiuc, M. D. (2022). Digital Transformation in Romanian Accounting Practice and Education: Impact

and Perspectives. Amfiteatru Economic, 24(59), 252-267. https://doi.org/10.24818/EA/2022/59/252

Hosseian Kashani, Z., Hajihasani, Z., Jahangirnia, H., & Gholami Jamkarani, R. (2021). Developing an Auditing

Documentation Quality Model Based on Grounded Theory Approach. Quarterly Journal of Financial Accounting

Research and Auditing, 13(52), 151-184. https://www.sid.ir/fa/Journal/ViewPaper.aspx?ID=578002

Izzo, M. F., Fasan, M., & Tiscini, R. (2021). The Role of Digital Transformation in Enabling Continuous Accounting

and the Effects on Intellectual Capital: The Case of Oracle. Meditari Accountancy Research.

https://doi.org/10.1108/MEDAR-02-2021-1212

Kamali Dolatabadi, M., & Darabi, R. (2022). The Role of Accounting Information Systems in Management and Cost

Reduction. Future Studies and Policy-Making, 8(26), 134-162. https://civilica.com/doc/1703907/

Pandey, N., Nayal, P., & Rathore, A. S. (2020). Digital Marketing for B2B Organizations: Structured Literature Review

and Future Research Directions. Journal of Business & Industrial Marketing. https://doi.org/10.1108/JBIM-06-

-0283

Sabuncu, B. (2022). The Effects of Digital Transformation on the Accounting Profession. Ömer Halisdemir Üniversitesi

İktisadi Ve İdari Bilimler Fakültesi Dergisi, 15(1), 103-115. https://doi.org/10.25287/ohuiibf.974840

Saghafi, A., & Jamalianpour, M. (2018). Technology, Blockchain, and the Future of Accounting and Auditing.

Accountant Journal, 34(2), 9-15. https://hesabdar.iica.ir/files/pdf/1397/3/hesabdar-1397-3-314-9-15.pdf

Sandner, P., Lange, A., & Schulden, P. (2020). The Role of the CFO of an Industrial Company: An Analysis of the

Impact of Blockchain Technology. Future Internet, 12(8), 128. https://doi.org/10.3390/fi12080128

Stafie, G., & Grosu, V. (2022). Digital Transformation of Accounting as a Result of the Implementation of Artificial

Intelligence in Accounting. Romanian Journal of Economics, 54(1 (63)), 95-112.

https://journals.indexcopernicus.com/publication/4025478

Yigitbasioglu, O., Green, P., & Cheung, M. Y. D. (2022). Digital Transformation and Accountants as Advisors.

Accounting, Auditing & Accountability Journal. https://doi.org/10.1108/AAAJ-02-2019-3894

Ziyadin, S., Suieubayeva, S., & Utegenova, A. (2019). Digital Transformation in Business. International Scientific

Conference "Digital Transformation of the Economy: Challenges, Trends, New Opportunities",

Downloads

Published

Submitted

Revised

Accepted

Issue

Section

License

Copyright (c) 2024 Journal of Technology in Entrepreneurship and Strategic Management (JTESM)

This work is licensed under a Creative Commons Attribution-NonCommercial 4.0 International License.