Presenting a Model of Professional and Organizational Identity of Internal Auditors and Examining Its Influencing Factors

Keywords:

professional identity, social identity theory, organizational identity, internal auditorAbstract

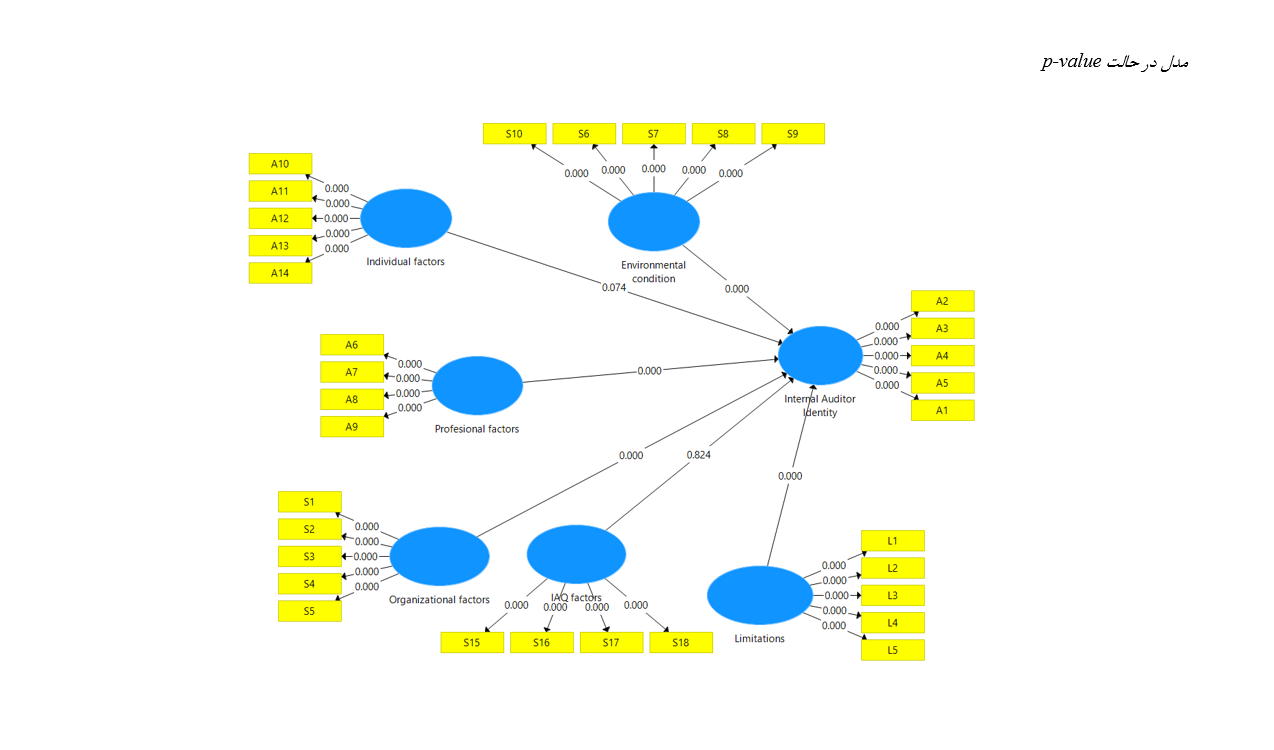

The rapid expansion of economic entities, advancements in communication technologies, and conflicts of interest have heightened the need for enhanced oversight mechanisms. In any profession, a sense of identity is a crucial aspect for those engaged in it. Auditors who are deeply involved in their profession view auditing as a significant component of their personal identity. This study employed a mixed-methods approach (qualitative and quantitative) based on the nature of data collection. In the qualitative phase, grounded theory was applied, and through theoretical and purposive sampling, 34 experts and key informants in the field of internal auditing were interviewed. The collected data were analyzed into 43 subcategories and 10 abstract categories. Subsequently, the factors influencing the identity of internal auditors were examined in the quantitative phase using structural equation modeling and SmartPLS software.

The study’s findings revealed that internal auditors’ identity is significantly influenced by board-dependent causal factors. According to the proposed identity model of internal auditors, four main dimensions affect the formation of their identity within organizations: factors related to the individuality of the internal auditor, the profession, the organization, associations, and the quality of internal audit work. Overall, internal and external, as well as environmental factors, were identified as crucial in shaping their identity. Additionally, the context and background for forming the identity of internal auditors were introduced in two dimensions: the economic conditions of the country and challenges stemming from the lack of oversight. The outcomes of identity formation for auditors included ethical implications, control enhancement, and accreditation of their identity within organizations. Furthermore, the results of hypothesis testing in the quantitative phase indicated that professional, organizational, environmental conditions, and constraints had significant effects on the identity of internal auditors. However, individual factors and the quality of internal auditors had no significant impact on their identity.

Downloads

References

Antoh, A., Sholihin, M., Sugiri, S., & Arifa, C. (2024). A perspective on the whistleblowing intention of internal auditors: An integrated ethical decision-making model. Cogent Business & Management, 11(1). https://doi.org/10.1080/23311975.2023.2292817

Ashforth, B. E., Harrison, S. H., & Sluss, D. M. (2014). Becoming: the interaction of socialization and identity in organizations over time. London: Psychology Press. https://www.researchgate.net/publication/286458253_Becoming_The_interaction_of_socialization_and_identity_in_organizations_over_time

Brouard, F., Bujaki, M., Durocher, S., & Neilson, C. (2016). Professional Accountants' Identity Formation: An Integrative Framework. Journal of Business Ethics, 22(1), 142-153. https://doi.org/https://doi.org/10.1007/s10551-016-3157-z

Czerniawski, G. (2023). Professional development or professional learning: developing teacher educators' professional expertize. In R. J. Tierney, F. Rizvi, & K. Ercikan (Eds.), International Encyclopedia of Education (Fourth Edition) (pp. 469-474). Elsevier. https://doi.org/10.1016/B978-0-12-818630-5.04050-1

De Zwart, F. (2022). The Internal Audit Function. In The Key Code and Advanced Handbook for the Governance and Supervision of Banks in Australia. Springer. https://doi.org/10.1007/978-981-16-1710-2

Desi Lastianti, S., Muryani, E., & Ali, M. (2018). The Role of The Internal Audit Management of Enterprise Risk Management. International Journal of Entrepreneurship and Business Development, 1(2). https://www.researchgate.net/publication/324563296_The_Role_of_The_Internal_Audit_Management_of_Enterprise_Risk_Management

Djogo, Y. O. (2023). Internal Auditor Human Resources Development Strategy in the Era of Disruption. Atestasi Jurnal Ilmiah Akuntansi, 6(2), 627-639. https://doi.org/10.57178/atestasi.v6i2.723

Hamza, M., Alkabbji, R., Almbydeen, T. H., Almubaydeen, A., & Bajunaid, K. (2023). The Impact of Applying Electronic Internal Auditing in Raising the Efficiency of Financial Performance in Jordanian Commercial Banks. In B. A. M. Alareeni & I. Elgedawy (Eds.), Artificial Intelligence (AI) and Finance. Springer. https://doi.org/10.1007/978-3-031-39158-3_49

Lee, M. Y., & Kutty, F. M. (2023). Emotional Intelligence and Professional Identity of Student Teachers During Practicum. International Journal of Academic Research in Business and Social Sciences, 13(4). https://doi.org/10.6007/ijarbss/v13-i4/16736

Mashayekhi, B., Noroush, I., Hajazi, R., & Momeni Yanesari, A. (2019). Towards a Theory for the Process of Internal Auditors' Professional Identity Formation. Accounting and Management Knowledge, 8(29), 15-42. https://www.magiran.com/paper/1951946/towards-a-theory-for-internal-auditors-professional-identity-formation-process-in-iran?lang=en

Molaei, A. (2024). Organizational Environment and Whistleblowing Mindset Among Internal Auditors. Quarterly Journal of New Research Approaches in Management and Accounting, 8(92), 1996-2011. https://majournal.ir/index.php/ma/article/view/2630

Nikbakht, M., Rezaei, Z., & Menti, V. (2017). Designing an Internal Audit Quality Model. 17, 5-57. https://danesh.dmk.ir/article-1-1693-fa.html

Nour, A. N. I., & Tanbour, K. M. (2023). The Impact of the Code of Professional Conduct for Internal Auditors on the Effectiveness of Internal Auditing Units in Banks Listed on the Palestine Stock Exchange During COVID-19 Pandemic. In B. Alareeni & A. Hamdan (Eds.), Explore Business, Technology Opportunities and Challenges After the Covid-19 Pandemic. Springer. https://doi.org/10.1007/978-3-031-08954-1_45

Ostermeier, K., Anzollitto, P., Cooper, D., & Hancock, J. I. (2023). When Identities Collide: Organizational and Professional Identity Conflict and Employee Outcomes. Management Decision, 61(9), 2493-2511. https://doi.org/10.1108/md-07-2022-0971

Praja, R. A. (2024). The Influence of Human Resources Audit and Internal Control System on Employee Performance in PT. Subur Sedaya Maju Prabumulih. JuBIR, 2(2), 115. https://doi.org/10.31315/jubir.v2i2.7958

Taghavi, A., & Yaqubi Seini, S. H. (2018). Examining the Role of Internal Auditors in the Development and Growth of Iranian Stock Exchange Companies. Conference on Accounting and Management,

Thapa, A. (2023). Investigating the Essence of Organizational Identity: Perspectives From Employees in the Banking Sector of Nepal. Nepal Journal of Multidisciplinary Research, 6(4), 244-255. https://doi.org/10.3126/njmr.v6i4.62088

Xanthopoulou, A. (2024). The Effect of Internal Audit on Universities’ Reliability and Performance. 987-994. https://doi.org/10.1007/978-3-031-51038-0_106

Zhang, J. (2023). A Study on the Impact of Organizational Support on Employee Loyalty: Using Organizational Identity as a Mediation. The Euraseans Journal on Global Socio-Economic Dynamics(6(43)), 104-110. https://doi.org/10.35678/2539-5645.6(43).2023.104-110

Zhang, W. (2024). Regulatory Focus as a Mediator in the Relationship Between Nurses' Organizational Silence and Professional Identity. Journal of Advanced Nursing, 80(9), 3625-3636. https://doi.org/10.1111/jan.16113

Downloads

Published

Submitted

Revised

Accepted

Issue

Section

License

Copyright (c) 2025 Farzaneh Akhtarian (Author); Rezvan Hejazi; Mohammad Hossein Ranjbar, Hojatollah salari, Davoud khodadadi (Author)

This work is licensed under a Creative Commons Attribution-NonCommercial 4.0 International License.