Identification and Modeling of Factors Affecting the Effectiveness of Internal Auditing and Its Impact on Financial Reporting Quality Considering the Role of Organizational Culture

Keywords:

Effectiveness of internal audit, quality of financial reporting, organizational culture.Abstract

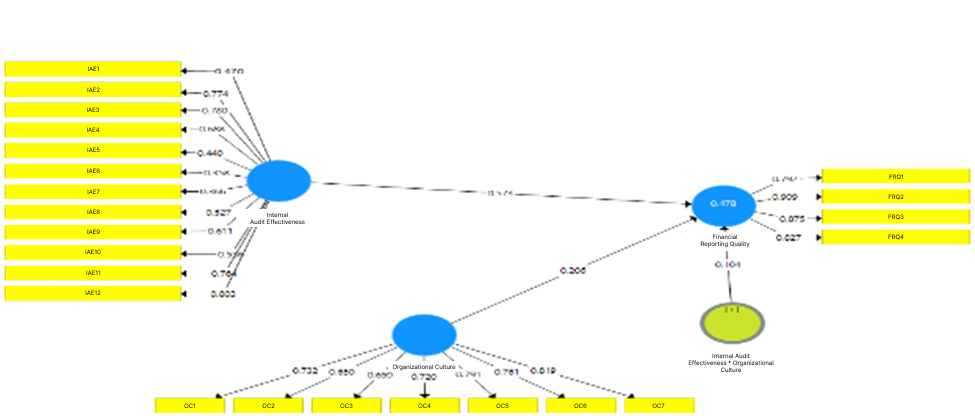

The primary objective of this study is to identify and model the factors influencing the effectiveness of internal auditing and its impact on financial reporting quality, taking into account the role of organizational culture. This research is exploratory in nature and is classified as applied research in terms of its purpose. The statistical population consists of 179 managers from listed and over-the-counter (OTC) companies in Iran. Data collection was conducted using interviews and questionnaires, while hypothesis testing employed inferential statistics and structural equation modeling. The findings indicate that, in order of influence, organizational structure, risk management, audit committee, board of directors and executives, accounting information systems, working relationships (interactions) between internal and external auditors, independence, ethical courage, technological capabilities, professional commitment, auditor competence, and internal control have the most significant impact on the effectiveness of internal auditing. Moreover, the results demonstrate that both the effectiveness of internal auditing and organizational culture have a positive effect on financial reporting quality. Additional findings reveal that organizational culture does not have a moderating effect on the relationship between the effectiveness of internal auditing and financial reporting quality.

References

K. Barkhordar, A. Nazemi, and N. R. Namazi, "Investigating factors affecting the effectiveness of internal auditing and evaluating the role of internal auditing in risk management and internal controls in the Agricultural Bank," Professional Auditing Research Journal, vol. 1, no. 2, pp. 8-35, 2021.

M. Tajik Jalaeri, J. Ramazani, and Y. Kamyabi, "The impact of the international professional framework on the effectiveness of internal auditing," Financial Accounting and Auditing Research, vol. 14, no. 53, pp. 77-102, 2022.

G. Smith, "Communication Skills are Critical for Internal Auditors," Managerial Auditing Journal, vol. 20, no. 5, pp. 513-519, 2005, doi: https://doi.org/10.1108/02686900510598858.

D. F. Prawitt, J. L. Smith, and D. A. Wood, "Internal audit quality and earnings management," The Accounting Review, vol. 84, pp. 1255-1280, 2009, doi: https://doi.org/10.2308/accr.2009.84.4.1255.

O. Bamari, M. R. Shorvarzi, and Z. Noori Topkanlou, "Investigating and explaining the relationship between internal auditing and the quality of financial reporting," Accounting and Auditing Management Knowledge, vol. 14, no. 53, pp. 291-304, 2024.

D. A. Nugroho, R. Sari, and C. Kuntadi, "Factors Affecting Fraud Prevention: Organizational Culture, Human Resource Competence and the Role of The Internal Auditor," Dinasti International Journal of Education Management and Social Science, vol. 4, no. 4, pp. 627-636, 2023.

I. E. Albawwat, M. E. Al-hajaia, and Y. S. Al frijat, "The Relationship Between Internal Auditors' Personality Traits, Internal Audit Effectiveness, and Financial Reporting Quality: Empirical Evidence from Jordan," The Journal of Asian Finance, Economics and Business, vol. 8, no. 4, pp. 797-808, 2021.

S. S. Halbouni, "The role of auditors in preventing, detecting, and reporting fraud: The case of the United Arab Emirates (UAE)," International Journal of Auditing, vol. 19, no. 2, pp. 117-130, 2015, doi: https://doi.org/10.1111/ijau.12040.

J. Stewart and N. Subramaniam, "Internal audit independence and objectivity: emerging research opportunities," Managerial Auditing Journal, vol. 25, no. 4, pp. 328-360, 2010, doi: https://doi.org/10.1108/02686901011034162.

M. Afzali, "Corporate culture and financial statement comparability," Advances in Accounting, vol. 60, p. 100640, 2023, doi: https://doi.org/10.1016/j.adiac.2022.100640.

H. Ahmadi, H. Valipour, and G. R. Jamali, "The impact of cultural intelligence of financial managers on the quality of financial reporting in companies," Journal of Financial Management Strategy, vol. 11, no. 4, pp. 197-218, 2023.

L. J. Abbott, B. Daugherty, S. Parker, and G. F. Peters, "Internal Audit Quality and Financial Reporting Quality: The Joint Importance of Independence and Competence," Journal of Accounting Research, vol. 54, pp. 3-40, 2016, doi: https://doi.org/10.1111/1475-679X.12099.

B. Jaggy, S. Mitra, and M. Hosain, "Earnings quality, internal control, weaknesses and industry specialist audits," Review of Quantitative Finance and Accounting, vol. 45, no. 1, pp. 1-32, 2015, doi: https://doi.org/10.1007/s11156-013-0431-3.

S. Lin, M. Pizzini, M. E. Vargus, and I. Bardhan, "The role of the internal audit function in the detection and disclosure of material weaknesses," The Accounting Review, vol. 86, no. 1, pp. 287-323, 2011, doi: https://doi.org/10.2308/accr.00000016.

A. Madawaki, A. Ahmi, and H. N. Ahmad, "Internal audit functions, financial reporting quality and moderating effect of senior management support," Meditari Accountancy Research, vol. ahead-of-print, pp. ahead-of-print, 2021, doi: https://doi.org/10.1108/MEDAR-04-2020-0852.

Q. Xu, G. D. Fernando, and K. Tam, "Trust and firm performance: A bi-directional study," Advances in Accounting, vol. 47, p. 100433, 2019, doi: https://doi.org/10.1016/j.adiac.2019.100433.

K. Sachin and K. Ravi, "Organizational Culture as a HR Strategy for Successful Knowledge Management," Strategic HR Review, vol. 11, 2012.

J. L. Altamuro, J. Gray, and H. Zhang, "Corporate Integrity Culture and Compliance: A Study of the Pharmaceutical Industry," Contemporary Accounting Research, vol. 39, no. 1, pp. 428-458, 2022, doi: https://doi.org/10.1111/1911-3846.12727.

Z. Khanam, "Effectiveness of internal auditing from the lens of internal audit factors: empirical findings from the banking sector of Bangladesh," Journal of Financial Crime, vol. ahead-of-print, pp. ahead-of-print, 2024, doi: https://doi.org/10.1108/JFC-11-2023-0299.

M. En-nejjari, H. El Aissaoui, and A. Lakhouil, "Evaluation of the effectiveness of internal audit in local authorities: Case of Moroccan communes," African Scientific Journal, vol. 3, no. 23, pp. 20-37, 2024.

Y. Jung and M. K. Cho, "Impacts of reporting lines and joint reviews on internal audit effectiveness," Managerial Auditing Journal, vol. 37, no. 4, pp. 486-518, 2022, doi: https://doi.org/10.1108/MAJ-10-2020-2862.

M. H. Alqaraleh, M. O. S. Almari, B. J. A. Ali, and M. S. Oudat, "The mediating role of organizational culture on the relationship between information technology and internal audit effectiveness," Corporate Governance and Organizational Behavior Review, vol. 6, no. 1, pp. 8-18, 2022, doi: https://doi.org/10.22495/cgobrv6i1p1.

A. Bhandari, B. Mammadov, M. Thevenot, and H. Vakilzadeh, "Corporate Culture and Financial Reporting Quality," Accounting Horizons, vol. 36, no. 1, pp. 1-24, 2022, doi: https://doi.org/10.2308/HORIZONS-19-003.

N. Hidayah, "The effects of internal control implementation and organizational culture on financial reporting quality," Religación. Revista de Ciencias Sociales y Humanidades, vol. 4, no. 16, pp. 236-244, 2019.

R. R. Gamayuni, "The Effect of Internal Audit Function Effectiveness and Implementation of Accrual Based Government Accounting Standard on Financial Reporting Quality," Review of Integrative Business and Economics Research, vol. 7, no. Supplementary Issue 1, pp. 46-58, 2018.

M. Riahi Nejad and A. Tavanegar, "The impact of organizational culture on the relationship between earnings management and the readability of financial reports," Financial Accounting and Auditing Research, vol. 13, no. 52, pp. 87-114, 2021.

M. Riahi Nejad and A. Tavanegar, "The impact of organizational culture on the readability of financial reports," Accounting and Auditing Research, vol. 14, no. 54, pp. 84-69, 2022.

S. Mohseni Nia and J. Babajani, "Investigating the impact of internal audit quality on the quality of financial reporting in companies listed on the Tehran Stock Exchange," Financial Accounting Research, vol. 12, no. 4, pp. 19-38, 2020.

Z. Hajiha and H. Jafarpoor, "The quality of internal audit performance, financial reporting, and audit efficiency in companies listed on the Tehran Stock Exchange," Auditing Knowledge, vol. 20, no. 79, pp. 47-70, 2020.

H. B. Nakhaei and S. Heydari Nasab, "The impact of internal audit performance quality and the audit committee on the quality of financial reporting in companies listed on the Tehran Stock Exchange," Accounting and Management Outlook, vol. 2, no. 14, pp. 42-56, 2019.

S. Datta, T. Doan, and F. Toscano, "Does firm culture influence corporate financing decisions? Evidence from debt maturity choice," Journal of Banking and Finance, vol. 169, p. 107310, 2024, doi: https://doi.org/10.1016/j.jbankfin.2024.107310.

A. Habibzadeh, "The impact of internal auditors on the quality of financial reporting with an emphasis on the role of the audit committee," Accounting and Management Outlook, vol. 3, no. 28, pp. 26-40, 2020.

Downloads

Published

Submitted

Revised

Accepted

Issue

Section

License

Copyright (c) 2025 Management Strategies and Engineering Sciences

This work is licensed under a Creative Commons Attribution-NonCommercial 4.0 International License.